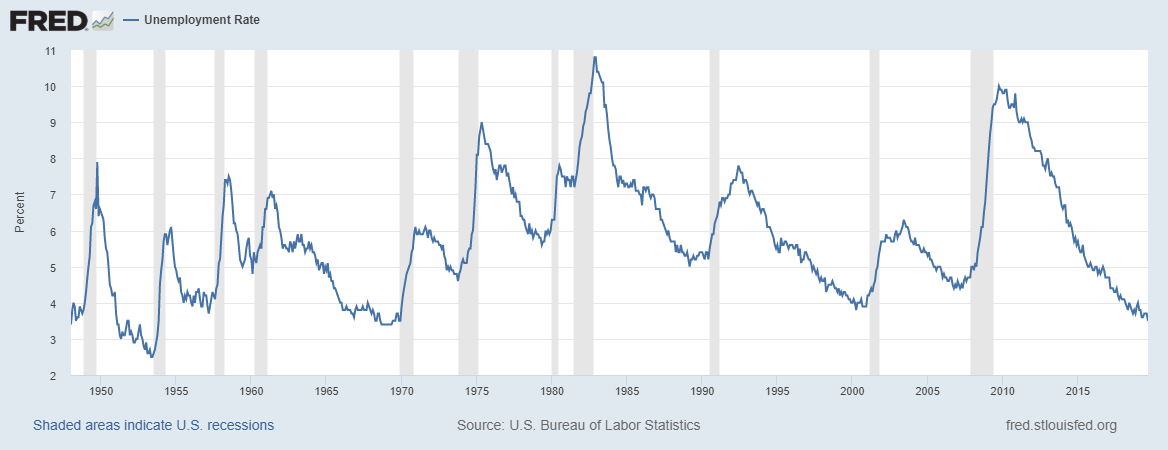

The Unemployment Rate is a subcomponent in the Economic cycle indicator in TJT’s proprietary InVEST Risk Model®.

U.S. unemployment hit a 50-year low in September. The jobless rate dropped to 3.5% in September from 3.7% in August, marking the lowest rate since December 1969.

Contact us to learn why this is important when managing your money.